The U.S. economy is heading into tax season with a sizable fiscal tailwind. Analysts at Bank of America Global Research say changes tied to the One Big Beautiful Bill Act (OBBBA) are expected to drive a sharp increase in tax refunds, injecting tens of billions of dollars into the economy compared with last year. The boost, however, is unlikely to be felt evenly—and could further widen the nation’s growing economic divide.

Bank of America estimates that tax refunds in 2026 will total about $65 billion more than in 2025, an 18% year-over-year jump. Overall, the consumer stimulus from the OBBBA is projected to reach between $135 billion and $140 billion. But the structure of the tax changes—particularly adjustments to the state and local tax (SALT) deduction cap—means that middle- and higher-income households are positioned to receive the largest gains.

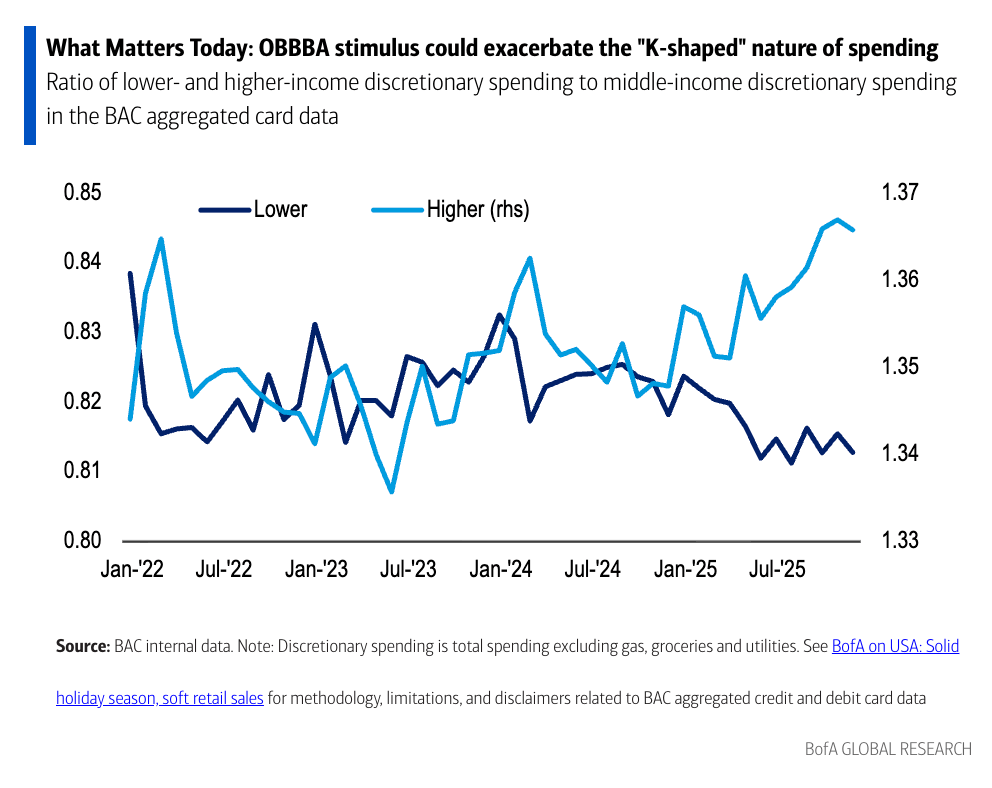

A widening “K-shaped” economy

The bank’s analysis underscores a persistent “K-shaped” pattern in the post-2025 economy, where higher-income households continue to pull away financially from lower-income Americans. In late 2025 and early 2026, spending among higher-income households rose 2.4%, compared with just 0.4% growth among lower-income households.

Middle- and higher-income earners are expected to be the primary beneficiaries of the new policy, according to senior U.S. economist Aditya Bhave, who warned that K-shaped spending dynamics could become even more pronounced. His assessment follows recent findings from the New York Federal Reserve showing that this economic divergence has been building for at least three years. “The consumer divide is about to get deeper,” Bhave said.

While the legislation includes deductions for tip and overtime income—provisions that help service workers—it also raises the SALT deduction cap, a move that disproportionately benefits higher earners. Estimates from the nonpartisan Tax Policy Center suggest the largest cash gains from the bill will flow to households at the top of the income spectrum.

Treasury and independent projections indicate that the typical tax refund in 2026 could be roughly $300 to $1,000 higher than last year, with some estimates placing the average refund near $3,800.

Wall Street versus Main Street

How this money moves through the economy matters. Bank of America notes that higher-income households are more likely to save than spend, meaning a significant share of the stimulus may never reach everyday retail activity. Roughly half of the additional funds, analysts say, could be diverted into savings or investments, with wealthier recipients more inclined to buy stocks than pay down debt.

That pattern is already evident. Throughout 2025, affluent consumers largely maintained spending on services, while the broader consumer base became more cautious—trading down to cheaper items and pulling back on big-ticket purchases such as furniture and electronics.

A lifeline for lower-income households

Even so, the refund surge could provide meaningful relief for lower-income families. Bank of America data show that tax refunds make up a far larger share of monthly spending for these households than for wealthier ones, increasing the likelihood that the money will be spent quickly.

“Even if refund growth were fairly uniform, it could still lift lower-income household spending and ease pressure on discretionary budgets,” noted a separate analysis from the Bank of America Institute. Historically, lower-income households boost spending on goods, travel, and leisure by nearly 40% in the weeks after receiving tax refunds.

The timing is critical. Fourth-quarter GDP tracking for 2025 has slipped to 2.4%, and the economy has experienced a choppy start to 2026. While the extra $65 billion in refunds should provide a short-term lift to discretionary spending between February and April, Bank of America cautions that sustained economic momentum will ultimately depend on the strength of the labor market.